Demystifying the Qualification Refine for an Equity Car Loan Approval

Browsing the certification process for an equity car loan approval can often seem like analyzing a complicated puzzle, with numerous aspects at play that identify one's eligibility. From rigorous credit history demands to thorough home assessments, each action holds significance in the lending institution's decision-making process. Recognizing the interaction in between debt-to-income ratios, loan-to-value proportions, and other vital requirements is paramount in protecting authorization for an equity funding. As we delve much deeper right into the ins and outs of these needs, a clearer course emerges for potential consumers seeking monetary leverage with equity car loans.

Secret Qualification Criteria

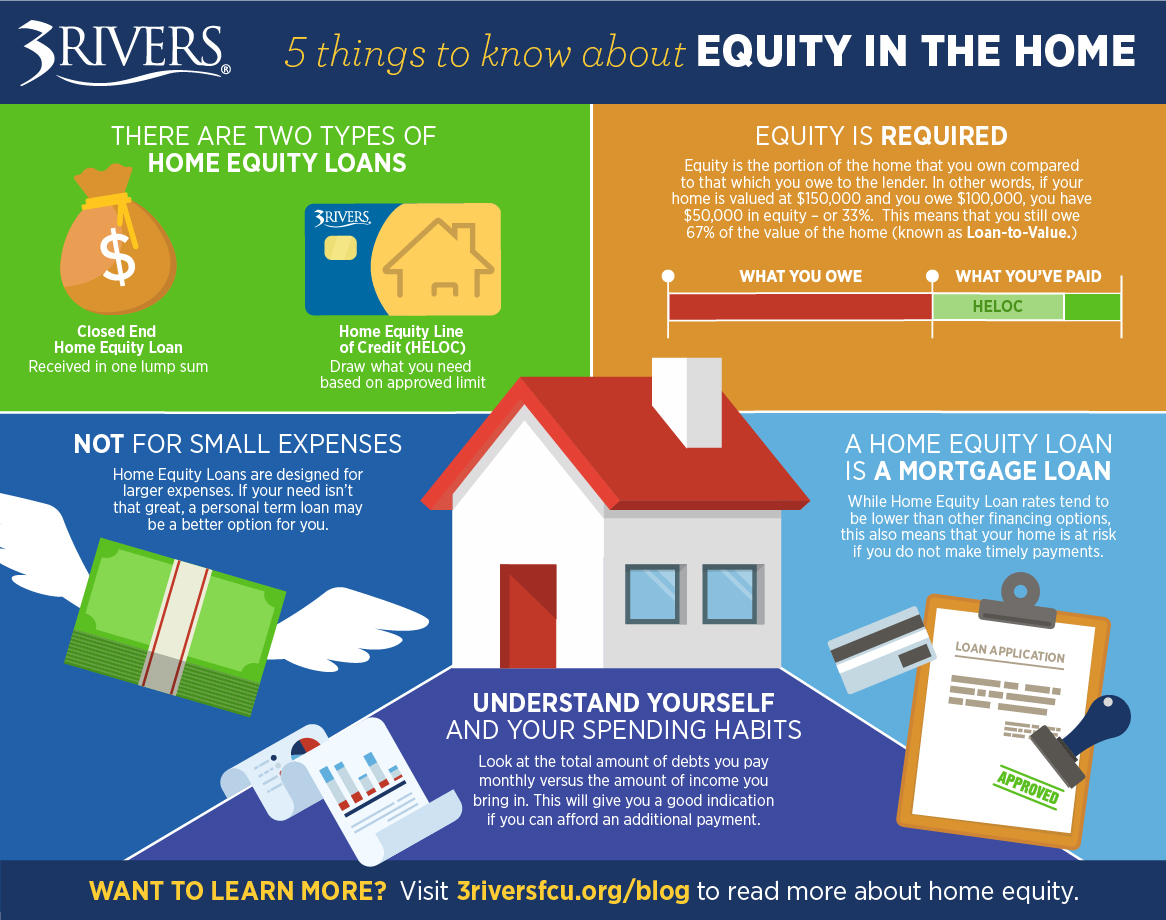

To receive an equity loan approval, meeting details essential qualification criteria is vital. Lenders commonly require applicants to have a minimal credit rating, frequently in the series of 620 to 700, relying on the organization. A strong credit rating, revealing a liable settlement track record, is also essential. Additionally, lenders assess the applicant's debt-to-income ratio, with most preferring a ratio listed below 43%. This shows the consumer's ability to take care of added financial debt sensibly.

Moreover, lending institutions review the loan-to-value ratio, which compares the quantity of the funding to the assessed worth of the residential or commercial property. Usually, loan providers prefer a reduced ratio, such as 80% or much less, to reduce their risk. Work and income security are essential factors in the authorization process, with lending institutions seeking guarantee that the debtor has a trustworthy source of income to settle the finance. Satisfying these vital eligibility standards enhances the likelihood of protecting approval for an equity finance.

Credit Rating Relevance

Lenders usually have minimal credit score demands for equity car loans, with ratings over 700 generally thought about excellent. By maintaining a great credit score with prompt bill repayments, reduced credit scores use, and responsible loaning, candidates can boost their opportunities of equity funding approval at competitive rates.

Debt-to-Income Ratio Analysis

Given the important function of debt ratings in identifying equity loan authorization, another crucial element that lending institutions analyze is a candidate's debt-to-income proportion analysis. The debt-to-income ratio is an essential monetary statistics that gives understanding into an individual's capability to handle extra financial obligation responsibly. Lenders compute this proportion by dividing the total month-to-month debt obligations of an applicant by their gross month-to-month earnings. A lower debt-to-income ratio suggests that a customer has more revenue offered to cover their financial obligation repayments, making them a more eye-catching candidate for an equity financing.

Lenders typically have specific debt-to-income proportion requirements that consumers should fulfill to qualify for go to website an equity financing. While these demands can differ amongst lenders, a typical benchmark is a debt-to-income proportion of 43% or reduced. Customers with a greater debt-to-income proportion may deal with obstacles in securing approval for an equity financing, as it suggests a higher danger of back-pedaling the funding. Equity Loans. It is crucial for applicants to evaluate and possibly decrease their debt-to-income ratio before applying for an equity car loan to boost their possibilities of approval.

Home Appraisal Requirements

Assessing the value of the residential property with a detailed evaluation is a fundamental action in the equity financing authorization process. Lenders require a home appraisal to ensure that the home gives adequate collateral for the lending quantity asked for by the customer. Throughout the building evaluation, a certified appraiser reviews different factors such as the property's problem, size, area, comparable building worths in the area, and any type of unique attributes that may influence its general well worth.

The home's appraisal worth plays a vital role in figuring out the optimum amount of equity that can be obtained against the home. Lenders commonly need that the evaluated value fulfills or goes beyond a specific percent of the funding quantity, known as the loan-to-value ratio. This proportion helps minimize the lender's danger by guaranteeing that the home holds adequate value to cover the financing in case of default.

Inevitably, a comprehensive building appraisal is necessary for both the borrower and the lender to properly assess the home's worth and determine the expediency of providing an equity lending. - Home Equity Loan

Comprehending Loan-to-Value Ratio

The loan-to-value proportion is a key economic metric utilized by lenders to examine the threat connected with giving an equity funding based on the building's appraised worth. This proportion is calculated by splitting the amount of the lending by the assessed worth of the home. If a property is assessed at $200,000 and the finance quantity is $150,000, the loan-to-value ratio would be 75% ($ 150,000/$ 200,000)

Lenders utilize the loan-to-value ratio to identify the degree of threat they are taking on by offering a finance. A greater loan-to-value ratio indicates a higher risk for the loan provider, as the debtor has much less equity in the building. Lenders typically prefer lower loan-to-value ratios, as they provide a cushion in case the consumer defaults on the car loan and the residential property requires to be marketed to recuperate the funds.

Debtors can likewise benefit from a lower loan-to-value ratio, as it may cause far better financing terms, such as reduced rates of interest or minimized charges (Alpine Credits Canada). Understanding the loan-to-value ratio is vital for both lending institutions and consumers in the equity loan authorization procedure

Verdict

In final thought, the credentials procedure for an equity lending authorization is based on essential qualification requirements, credit scores rating value, debt-to-income ratio analysis, home appraisal demands, and understanding loan-to-value ratio. Recognizing these elements can assist people navigate the equity financing approval procedure more efficiently.

Recognizing the interplay between debt-to-income proportions, loan-to-value ratios, and other vital criteria is vital in safeguarding approval for an equity financing.Provided the important role of credit score scores in identifying equity finance authorization, another vital facet that lenders evaluate is a candidate's debt-to-income proportion evaluation - Alpine Credits Equity Loans. Consumers with a higher debt-to-income ratio might encounter challenges in protecting authorization for an equity lending, as it suggests a greater threat of defaulting on the finance. It is important for candidates to evaluate and potentially lower their debt-to-income proportion prior to using for an equity lending to enhance their opportunities of authorization

In verdict, the qualification process for an equity funding authorization is based on vital eligibility requirements, debt rating importance, debt-to-income ratio analysis, residential property assessment needs, and recognizing loan-to-value proportion.

Comments on “Home Equity Loan Conveniences: Why It's a Smart Financial Relocate”